QR Code Payments Explained: How They Work and Why They Matter (Updated 2026)

QR code payments crossed record transaction volumes in 2025 and are now infrastructure, not novelty. Understand how they work — merchant-presented vs consumer-presented, UPI, security, and what it means for your business. Updated June 2026.

QR code payments have revolutionized commerce in Asia and are rapidly expanding globally. The market exceeded $4.5 trillion in transaction volume in 2024 and is projected to grow 48% through 2029. From street vendors to luxury retailers, QR codes enable instant payments with minimal infrastructure.

This guide explains how QR code payments work, compares different systems, and helps you understand this increasingly important payment method.

How QR Code Payments Work

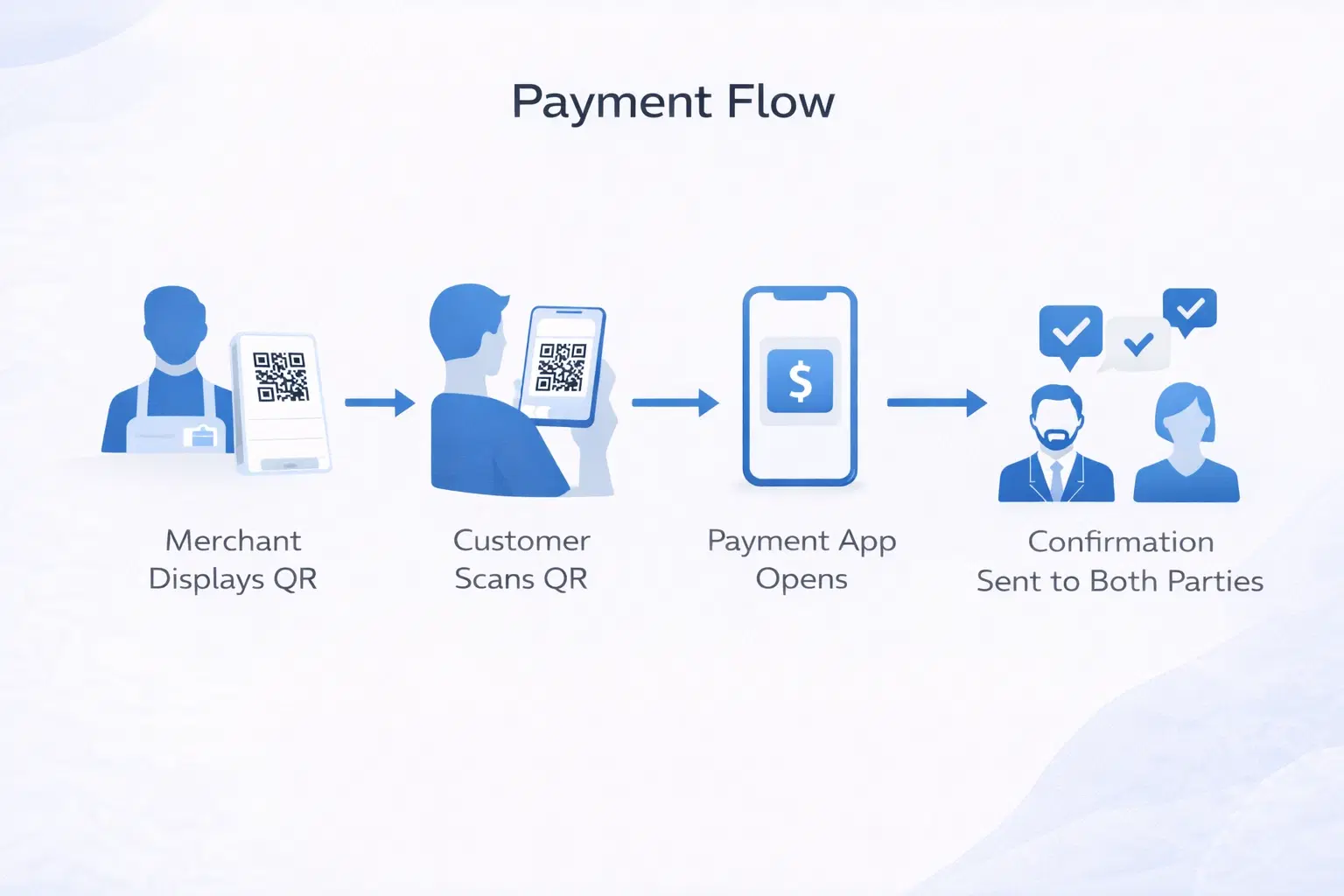

The basic flow is simple but the technology behind it is sophisticated:

The fundamental process: 1. A QR code contains payment information 2. A smartphone scans and decodes the information 3. A payment app processes the transaction 4. Funds transfer from buyer to seller

What's encoded in the QR code:

- Merchant identifier

- Payment amount (if static) or reference

- Payment network/processor information

- Transaction reference number

Two main approaches:

Merchant-Presented QR (MPM): Merchant displays code, customer scans to pay. Common at retail checkouts and restaurants.

Consumer-Presented QR (CPM): Customer displays code from their app, merchant scans. Common at chain retailers with POS systems.

Merchant-Presented QR Codes

The most common form globally:

Static QR codes:

- Printed, permanent code at checkout

- Customer enters payment amount manually

- Lowest cost implementation

- Best for: Small businesses, market vendors

Dynamic QR codes:

- Generated per transaction with exact amount

- Customer confirms and authorizes

- Reduces errors and fraud

- Best for: Established businesses, higher values

Advantages:

- Minimal infrastructure required (just printed code)

- No expensive POS hardware needed

- Works with multiple payment apps

- Easy to set up and maintain

Limitations:

- Customer must have compatible payment app

- Manual amount entry with static codes

- Less control over transaction flow

- May require internet on customer device

Consumer-Presented QR Codes

Used by major retailers and payment networks:

How it works: 1. Customer opens payment app 2. App generates unique QR code 3. Merchant scans with POS or scanner 4. Transaction processes automatically

Tokenization: The QR code doesn't contain actual payment credentials. Instead, it contains a token that references the customer's account securely.

Advantages:

- Customer credentials never exposed

- Works with existing POS infrastructure

- Faster checkout (no amount entry)

- Enhanced fraud protection

Examples in practice:

- Apple Pay / Google Pay in-app QR

- Walmart Pay

- Starbucks app

- Many Asian super-apps (WeChat, Alipay)

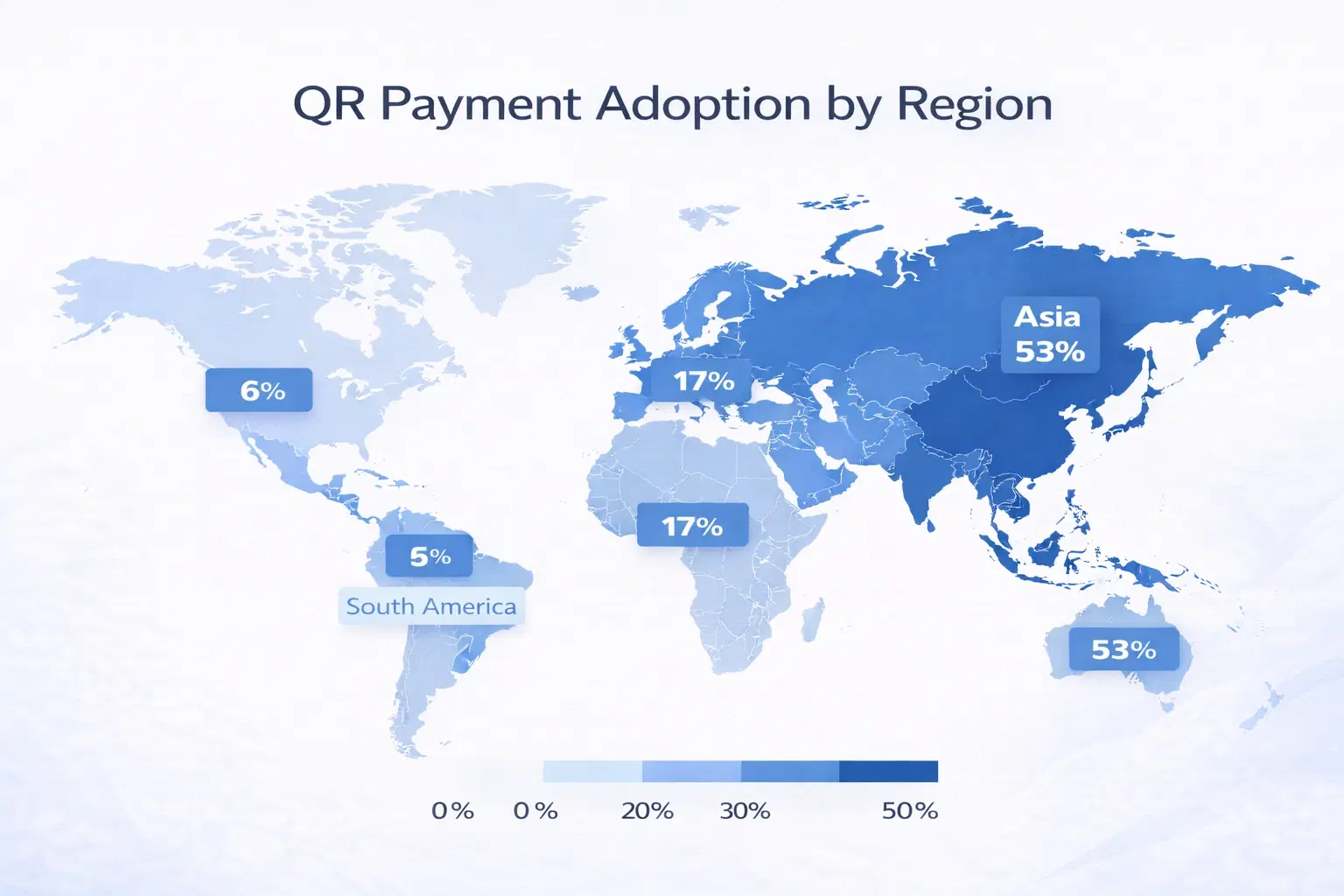

Global Adoption Landscape

QR payments adoption varies dramatically by region:

Asia-Pacific (Leading adoption):

- China: Ubiquitous via WeChat Pay and Alipay

- India: Rapid growth through UPI and BharatQR

- Southeast Asia: GrabPay, GCash, regional players

- Japan: PayPay, Line Pay gaining ground

North America and Europe (Growing):

- PayPal and Venmo QR codes

- Square and Stripe integrations

- Restaurant table ordering post-pandemic

- P2P payments between individuals

Latin America (Emerging):

- Brazil's Pix system

- MercadoPago in multiple countries

- Traditional banks adding QR features

Key adoption drivers:

- Smartphone penetration

- Banking/unbanked population ratio

- Existing payment infrastructure

- Regulatory support

- Network effects (critical mass)

Security Considerations

QR payments include multiple security layers:

Built-in protections:

- Tokenization (no real credentials in code)

- Dynamic codes that expire quickly

- Encryption of transmitted data

- Device-level authentication (fingerprint, face)

User-side security:

- App requires authentication to display code

- Transaction limits configurable

- Real-time notifications

- Easy dispute/freeze capability

Merchant-side security:

- Instant transaction verification

- No card skimming risk

- Digital audit trail

- Chargeback protection (varies)

Risks to watch:

- QR code overlay scams (fraudulent stickers)

- Phishing via fake payment pages

- Session hijacking on compromised devices

- Social engineering (fake "payment failed" messages)

Mitigation strategies:

- Verify QR codes aren't overlaid/tampered

- Only use official payment apps

- Enable transaction notifications

- Review transactions regularly

Important

Be cautious of QR codes for payments in public spaces. Criminals have been known to place fake codes over legitimate ones, especially on parking meters and vending machines.

Business Implementation Options

Multiple paths to accepting QR payments:

Option 1: Payment processor integration Work with your existing payment processor (Stripe, Square, etc.) to enable QR code payments. Usually the simplest path.

Option 2: Digital wallet direct Accept specific wallets like PayPal, Venmo, or regional options directly. May require multiple integrations.

Option 3: Bank-provided solutions Many business bank accounts now include QR payment acceptance. Check with your bank.

Option 4: Aggregator platforms Services that accept multiple QR payment types through one integration.

Implementation considerations:

- Transaction fees (compare to card processing)

- Settlement timing

- Integration complexity

- Customer payment app availability

- International payment support

- Assess customer payment preferences

- Compare processor fees and features

- Evaluate integration requirements

- Plan for training and rollout

- Set up reporting and reconciliation

- Test thoroughly before launch

Future of QR Payments

The landscape continues to evolve:

Emerging trends:

Cross-border interoperability: Singapore and Thailand already have cross-border QR payment agreements. Expect more regional and global connections.

Super-app expansion: Apps that combine payments with messaging, shopping, and services are growing beyond Asia.

Central Bank Digital Currencies: CBDCs may use QR codes as a primary interface, potentially transforming the landscape.

Offline capability: Systems that work without real-time internet connectivity are emerging.

Biometric integration: Face/fingerprint confirmation at POS for QR-initiated payments.

What this means for businesses: QR payment acceptance is transitioning from competitive advantage to baseline expectation. Early adopters benefit from customer convenience and reduced processing costs.

Getting Started Checklist

For businesses considering QR payments:

Assessment phase:

- ☐Survey customers on payment preferences

- ☐Analyze current payment mix and costs

- ☐Identify target QR payment platforms

- ☐Evaluate competitor adoption

Planning phase:

- ☐Select payment processor/platform

- ☐Design customer experience flow

- ☐Plan staff training

- ☐Prepare marketing/customer education

- ☐Set up accounting integration

Implementation phase:

- ☐Configure payment accounts

- ☐Generate/deploy QR codes

- ☐Train staff on process and troubleshooting

- ☐Test transactions end-to-end

- ☐Soft launch with employee transactions

Post-launch:

- ☐Monitor transaction success rates

- ☐Gather customer feedback

- ☐Optimize based on learnings

- ☐Consider expanding platforms accepted

Conclusion

QR code payments represent a fundamental shift in how transactions occur. They are simpler for customers, cheaper for merchants, and now expected rather than novel. In India, UPI QR payments have become the default way millions transact daily, and globally adoption continues to accelerate.

2026 reality check: QR payments are no longer an emerging technology to evaluate. They are table stakes. The question for any business is not whether to accept QR payments, but how to do it well and securely. The same security awareness applies: the tampered-QR-sticker scam (a fake payment QR placed over a real one) is a documented threat, so businesses must regularly verify their displayed payment codes have not been replaced.

If you are an Indian merchant, the practical setup guide for UPI specifically, including static vs dynamic UPI codes and how to protect against tampering, is in our UPI payments guide for Indian merchants.

Related reading:

The technology is mature, secure when implemented properly, and proven at massive scale. For businesses, QR payment acceptance is now a baseline expectation, and pairing it with dynamic QR codes for your marketing means one consistent, trackable QR presence across both payments and promotion.

Create dynamic QR codes for your business with QRForever. Permanent, editable codes for menus, promotions, and customer engagement alongside your payment setup.

Explore QRForever Solutions

Ready to Create Your Own QR Codes?

Start creating dynamic QR codes for your business today. Track analytics, update content anytime, and never reprint again.

Related Articles

Dynamic vs Static QR Codes: Which One Should You Use? (Updated 2026)

The complete 2026 guide to dynamic vs static QR codes—when each type is right, the hidden costs of choosing wrong, and a decision framework you can apply in 60 seconds.

QR Codes That Never Expire: Why Most Free QR Codes Stop Working (Updated 2026)

Free QR codes often expire after 14–90 days, breaking printed materials and costing more in reprints than a paid plan ever would. Updated 2026 guide with platform expiry timelines and a step-by-step rescue plan.

QR Code Error Correction Levels Explained: L, M, Q, H (2026)

QR codes have four error correction levels (L, M, Q, and H) that decide how much damage a code can survive and still scan. Choosing the right one is the difference between a reliable code and one that fails. Here is a clear 2026 guide.